Introduction: The Retirement Story You’re Telling Yourself

Most people have a picture of retirement in their mind—freedom from work, financial security, and time to enjoy life. But for many, that picture is based more on assumptions than on solid planning.

The uncomfortable truth is that retirement can become either a financial fact or a financial fiction, depending on the decisions made long before the retirement date arrives.

This article explores the key factors that determine whether your retirement plans are realistic—and what you can do today to make sure your retirement story has a happy ending.

The Difference Between Hope and a Plan

Hope feels good, but it’s not a strategy.

A real retirement plan:

- Is based on numbers, not guesses

- Accounts for risk and uncertainty

- Adjusts as life changes

Fictional retirement plans rely on assumptions like:

- “I’ll work longer if I need to.”

- “The market will take care of it.”

- “My expenses will drop.”

Reality often disagrees.

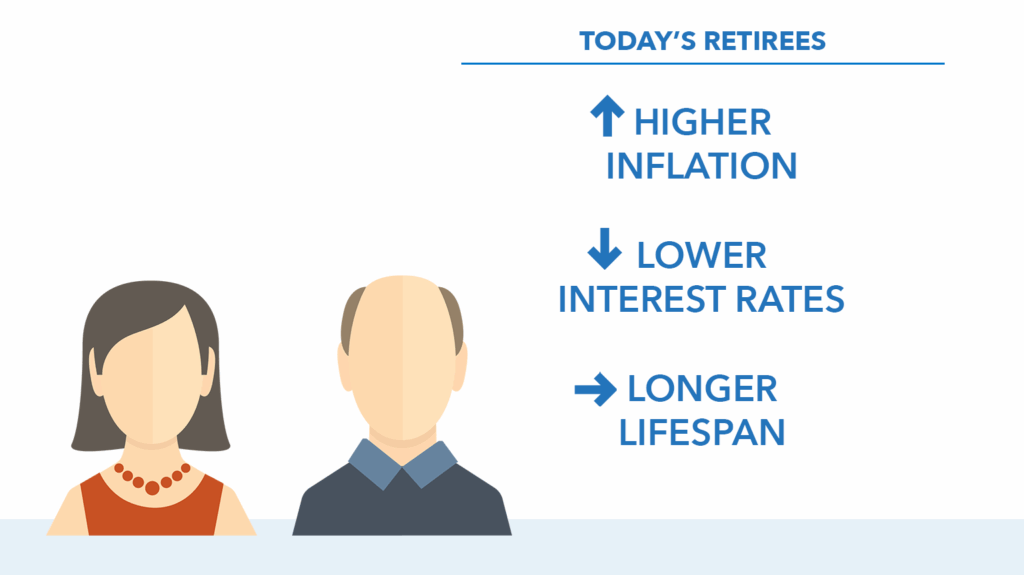

Longevity: The Retirement Timeline Keeps Growing

People are living longer than ever.

A longer life means:

- More years without earned income

- Greater healthcare expenses

- Increased inflation exposure

Without sufficient savings and growth, a long retirement can turn into a financial strain.

Inflation: The Silent Retirement Killer

Inflation doesn’t stop when you retire.

Over time, inflation:

- Reduces purchasing power

- Makes fixed incomes less reliable

- Raises everyday living costs

A retirement plan that ignores inflation risks becoming fiction quickly.

Income Sources: How Many Do You Really Have?

Many retirees rely too heavily on one or two income sources.

Common retirement income sources include:

- Government benefits

- Employer pensions

- Personal savings

- Investments

A strong plan spreads risk across multiple sources.

Investment Risk: Too Much or Too Little

Risk doesn’t disappear in retirement—it changes.

Common mistakes:

- Being too conservative too early

- Staying too aggressive too late

- Failing to rebalance

The right balance supports growth while protecting income.

Healthcare Costs: The Expense Few Plan For

Healthcare is one of the largest unknowns in retirement.

Costs may include:

- Insurance premiums

- Medications

- Long-term care

- Unexpected medical events

Ignoring healthcare planning can derail even strong retirement plans.

Taxes Don’t Retire When You Do

Many retirees are surprised by taxes.

Taxes may apply to:

- Retirement account withdrawals

- Investment income

- Social benefits

Tax planning can significantly affect how long your money lasts.

Withdrawal Strategy: How You Take Money Matters

Saving for retirement is only half the equation.

Without a withdrawal plan:

- Funds may be depleted too quickly

- Market downturns can cause lasting damage

- Taxes may increase unnecessarily

A strategy turns savings into sustainable income.

Emotional Decisions Can Turn Fact Into Fiction

Fear and overconfidence can destroy years of planning.

Examples include:

- Panic selling during market downturns

- Chasing high returns late in life

- Avoiding adjustments out of denial

Discipline and planning protect against emotional mistakes.

The Role of Regular Reviews

Retirement planning is not “set it and forget it.”

Life changes require:

- Portfolio adjustments

- Goal revisions

- Risk reassessment

Regular reviews keep plans grounded in reality.

Turning Retirement Fiction Into Fact

The good news: fiction can be rewritten.

Key steps include:

- Clarifying retirement goals

- Stress-testing assumptions

- Diversifying income

- Planning for healthcare and taxes

- Staying flexible and disciplined

Small actions today can change long-term outcomes.

Retirement Is a Process, Not an Event

Retirement success isn’t determined on your last day of work.

It’s shaped by:

- Consistent habits

- Thoughtful decisions

- Long-term discipline

Preparation beats prediction every time.

Final Thoughts: Write a Retirement Story Based on Reality

Your retirement doesn’t have to be a guess.

When planning is grounded in reality—not hope—retirement becomes a financial fact, not a financial fiction.

The question is not whether you want a comfortable retirement.

The question is whether your current plan supports the retirement you imagine.

The story is still being written—and you control the ending.

Word Count:

556

Summary:

It becomes more apparent each day that inflation has crept back into our lives even though government statistics may not support

this viewpoint. Rather, it’s the real world cost of food, drugs, fuel, utilities and education that indicate the inflationary trend.

If you’re like most Americans, your retirement account hasn’t grown much over the last 5 years. In fact, it’s been pretty flat

Keywords:

planning retirement,credit repair,idenity theft,plan retirement,home retirement,credit report repair,crdit repair service,bad credit repair

Article Body:

Keep Your Banking Information Safe

by Tomas Cullin

It would seem that the computer is becoming a bigger and bigger part of our lives each and every day. There’s good reason for that perception… it’s true. One specific area that is becoming incredibly popular is online banking. Customers love it because it is very convenient and a great time saver. The banks love it because it automates a great many functions for them and cuts down on their overhead.

The number one concern of anyone that deals with online banking should be security. Putting your personal information over the Internet can be risky, there is no denying that. Fraud and identity theft have become huge problems in the modern age. There are any number of hackers and thieves out there in cyberspace just waiting to prey on innocent people. They lurk in the deep spaces of the Internet just waiting for some of your private information that they can steal.

Fortunately for us, the financial institutions of the world are very aware of this problem and are working aggressively to combat it. There was a time when a bank’s chief security concern was whether they would be robbed or not. I think we’ve all seen the old movies about Bonnie & Clyde, John Dillinger and the like…to say nothing of the daring train robberies of the wild west. Now banks face a new and much deadlier challenge than ever before, and instead of wearing a mask and using a gun, the bad guys are now invisible and use keyboards. They can access information from the safety of their homes and apartments. And even at the local coffee shop through wireless connections.

Identity theft has now become so prevalent that thieves are rifling through garbage to attain any information that they can use to steal from their unsuspecting victims. With this said, there are some simple, common sense approaches that will go along way to securing personal bank information.

- Do not share your passwords with anyone and make sure if you write it done put it in a safe place where only you know where it is.

- Keep important documents locked in a safe or safety deposit box.

- Shred documents that you no longer need and use a cross cut shredder.

- If you bank online, make sure your bank is using a secure, encrypted site (It’s OK to ask what security features they employ). Make sure they use https in the address and you should see the lock symbol in the lower right hand corner of your browser.

- When using an ATM make sure no one can see the codes you enter.

These are a just a few of the things that can be done to keep banking information secure and to avoid possible crimes against you. While many of these suggestions seem to be glaringly obvious, all to many times they are taken for granted or just plain ignored. It is at these times when the criminals are at their best. Individuals that grow careless and complacent are exactly what criminals look for. Don’t be counted as one of the careless!

You may copy this article and place it on your own website, as long as you do not change it and include this resource box including the live link to the Credit Repair Advice site.

Tinggalkan Balasan